Thermal Coal Update

There have been some positive developments for the thermal coal thesis since my original post in March. As I mentioned in my last Iran War update, I’ve been adding exposure to this theme opportunistically, and have broadened the list of names to include Whitehaven ($WHC.AX), New Hope ($NHC.AX), CNR ($CNR), in addition to my original pick (Terracom ($TER.AX)). A detailed discussion of all these names is beyond the scope of this piece, but I do want to hit on the current macro picture.

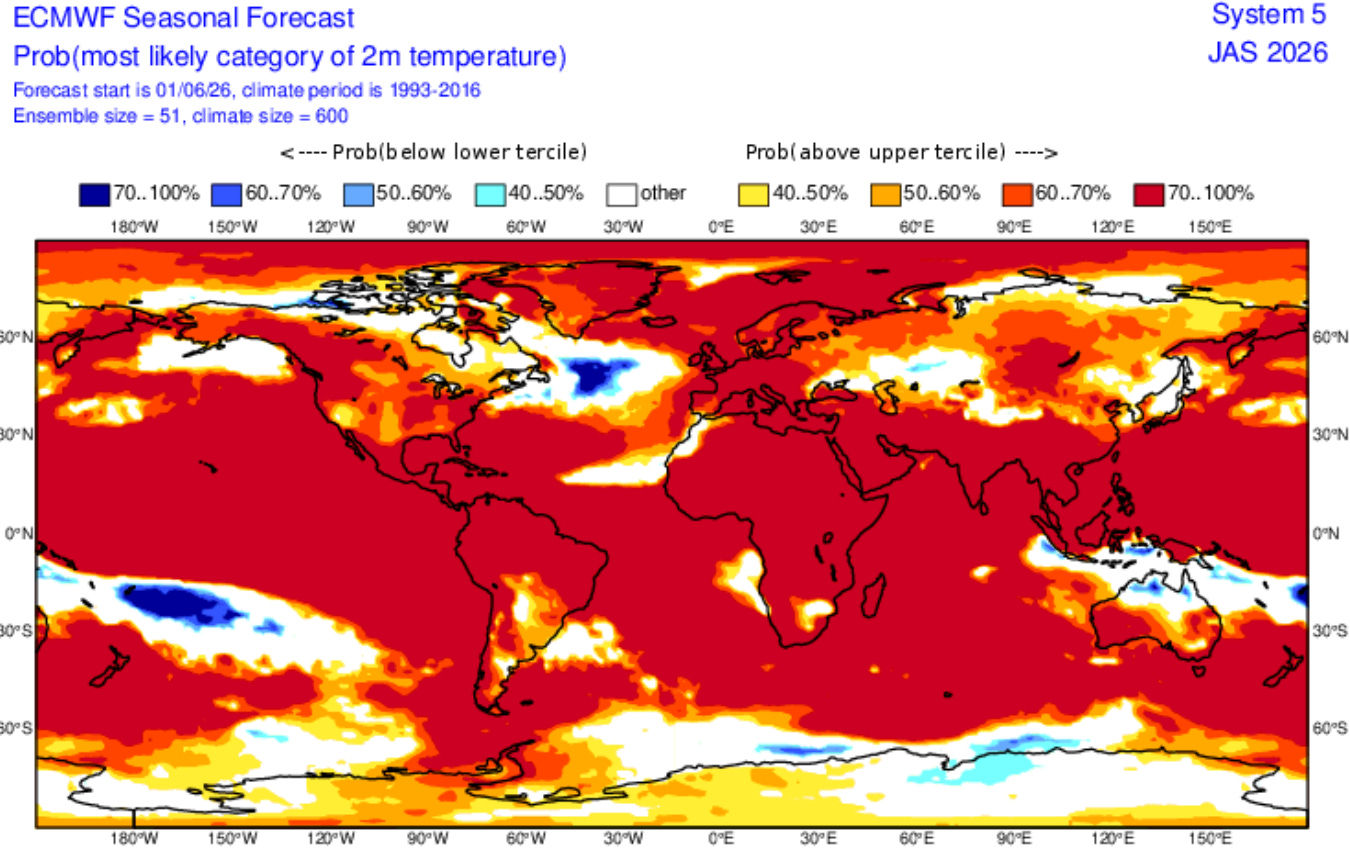

India is experiencing a significant heat wave, with peak electricity demand rising to all-time highs in excess of 270 GW. This pattern is expected to continue as weather forecasters are tracking an El Nino weather pattern that is likely to persist for the rest of this year. Sea surface temperatures in the equatorial Pacific are rising rapidly, and multiple forecast models suggest the current system could become the strongest El Nino in modern history.

El Nino is also likely to impact hydro generation as it historically weakens the South Asian monsoon season, and increases irrigation pumping demand. With 70% of Indian power generation coming from coal, domestic coal production struggling, and several power plants running low on inventory, the setup points to a sustained increase in thermal coal imports from India.

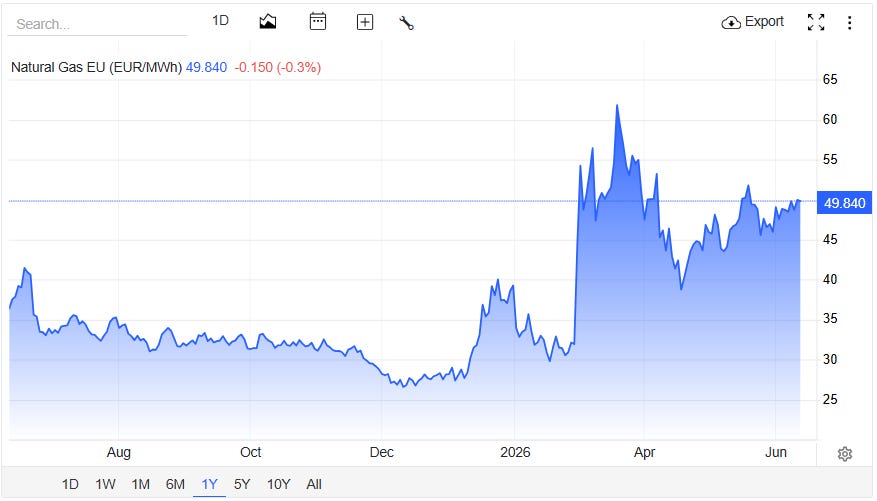

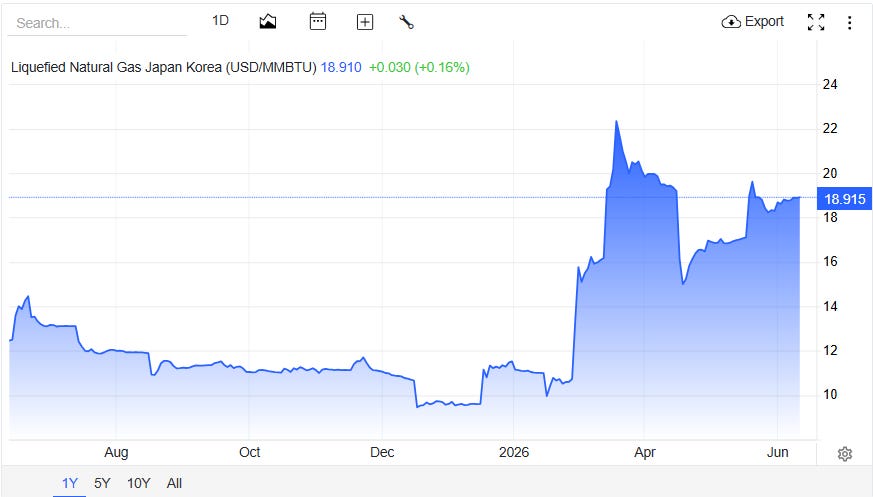

Meanwhile European (TTF) and Asian (JKM) gas prices remain elevated, and favor gas-to-coal switching. I laid out the math for this in my note from March. At the current JKM price, Asian buyers can justify paying $200/t+ for Newcastle (NEWC) coal. The switch is already happening, and prices are responding, with NEWC prices back to >$140/t after the recent dip to ~$120/t.

Rystad (energy consultancy) is reporting that Japan’s coal-fired generation is running +11% YoY. South Korean and Japanese coal imports were 50% and 20% above year-ago levels for May, respectively. China typically sees a drop in coal imports in June vs. May, but this year the data is tracking a m-o-m increase.

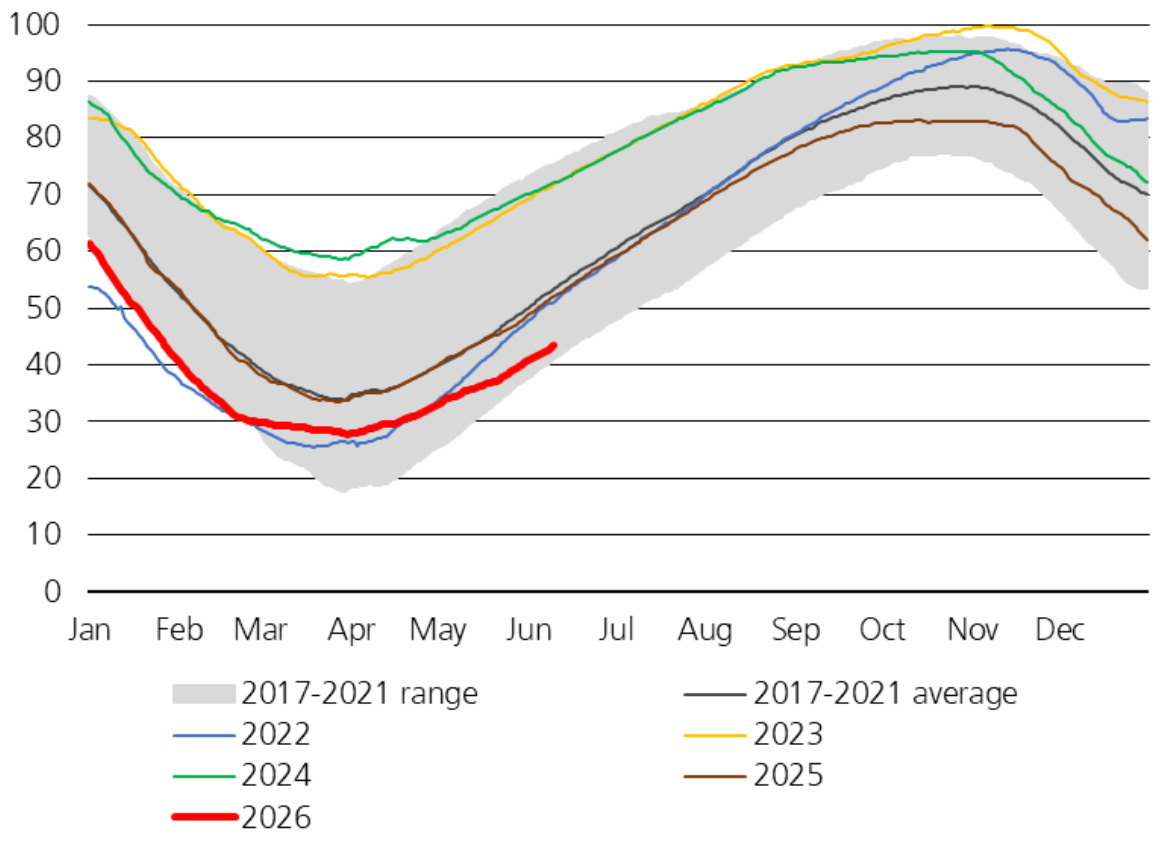

Gas inventories in Europe are running near 5-year lows, which could lead to a further boost for coal prices in Q3/Q4 if heating demand is higher than expected.

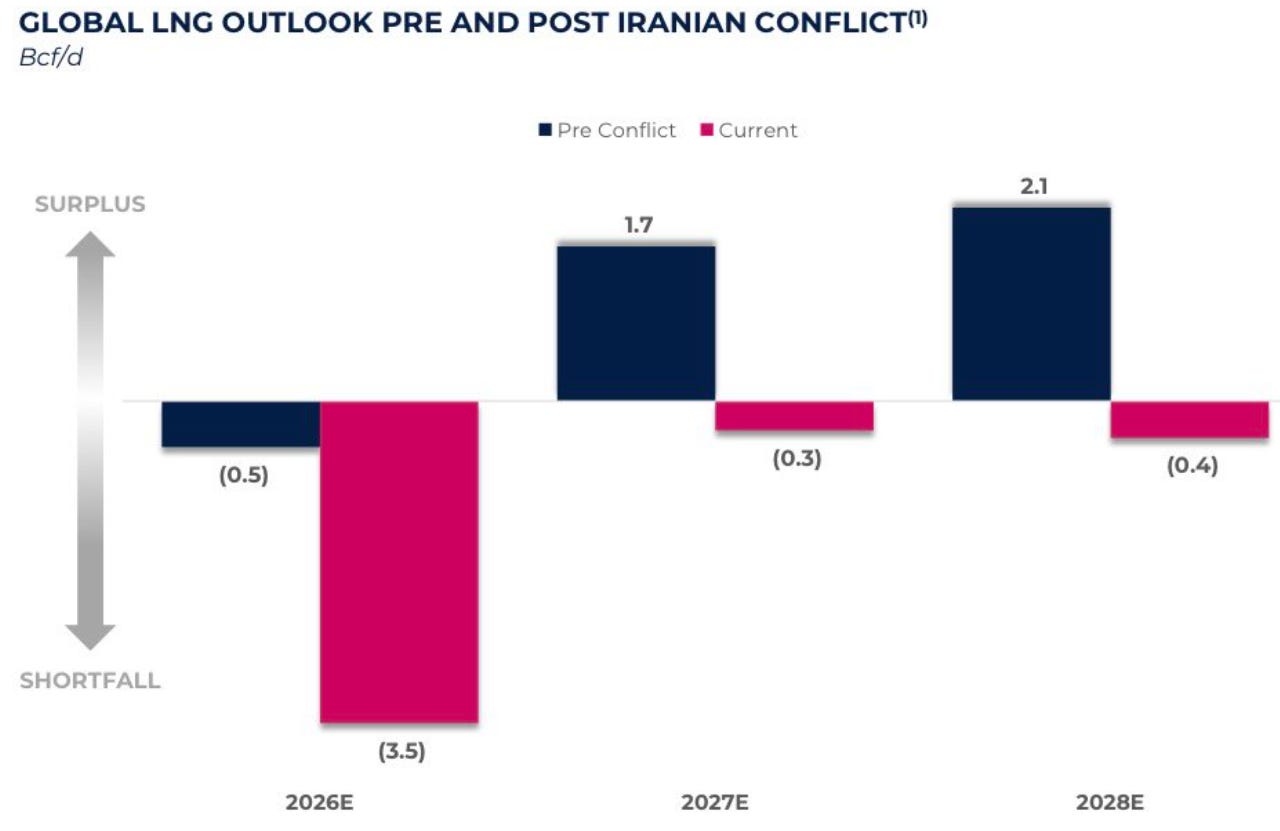

It’s becoming apparent that the disruption of LNG flows from Hormuz will have a long lasting impact on fuel buyers’ decision-making process going forward. After the Russia-Ukraine war in 2022, this is the second major disruption LNG buyers have faced. Unlike oil, LNG doesn’t have large commercial inventories or strategic reserves. Any disruption in flows means buyers have to scramble to secure alternate sources of energy.

Qatar was expected to bring online a number of significant LNG capacity additions, but these projects are now at risk. Work has been suspended at all 3 major LNG expansion projects (North Field East, West and South). NFE (32 mtpa) could be delayed for more than a year. NFS (16 mtpa) has been suspended indefinitely. NFW is also suspended, with no clear updates on status. As a result, the global LNG market has gone from projecting large surpluses in the coming years to now being largely balanced post the conflict.

The supply side for coal also supports higher prices. Indonesia, which accounts for nearly 50% of thermal coal exports, is restricting exports. Indonesian exports fell 26% YoY in May, representing the fifth consecutive drop. Thermal coal remains on the blacklist for financing and investment due to ESG concerns, and global supply is expected to contract. Outside of China, India and Indonesia, almost no new greenfield thermal coal mines have been project-financed. The number of new coal mines opened fell from 90 in 2024 to 30 in 2025.

Combine this with the fact that new coal plant additions are outstripping retirements even before the war started, and you can see why the case for sustained high thermal coal prices is strong.

As an investor who looks for asymmetric setups and margin of safety, what attracts me to the thesis is that at current valuations, one doesn’t need to make heroic assumptions regarding future coal prices to earn adequate returns on the coal mining stocks. At the current coal price, the names in my coal basket are trading at <4x EBITDA, which means investors are getting a significant portion of the mine reserve life for free.

I believe there are two ways to make money here:

If the Hormuz situation doesn’t resolve by the end of the summer or fall months, we are likely to see energy prices spike even higher. Coal prices and coal stocks could go parabolic, similar to the summer of 2022.

If the US and Iran reach an agreement and we see a gradual reopening of the Strait, we’ll likely see a near-term flush lower across the energy sector, including the coal names. But after the initial move lower, coal can still do well as the seasonal demand surge in Asia plays out (boosted by El Nino), and due to the longer-term structural factors discussed above.

LNG flows will likely take a longer time to normalize even if the Strait was opened.

Qatar Energy has already extended its force majeure to mid-August.

In a post-Iran War world, fuel buyers will likely diversify fuel sources and rely more on back up coal generation capacity.

What started out as a short-term / tactical trade is now evolving into a longer-term core holding for the portfolio. I started with a 4-5% NAV position, but coal names are now ~15% of the portfolio, and I continue to add on dips. Important data points to watch out for are India’s coal stockpiles and imports, evidence of continued gas to coal switching in Asia, and Europe pivoting to coal, especially as the winter months approach.

Awesome, im in NHC, love the write up.