The Opportunity In Offshore Drilling

A long-cycle energy investment

The offshore oil drilling industry has been through a painful downcycle that started in 2015/16 and worsened during COVID / 2020. The 2009 - 2014 period was a golden period for the industry: oil prices were high and the oil industry was worried about peak oil supply, which meant that E&Ps were willing to invest in long-term offshore contracts at high dayrates.

The advent of US shale and the ESG movement however ushered in a new period of uncertainty. Producers became unwilling to invest in offshore as the prospects of abundant US shale oil production at $50 - $60 / bbl (“shale band”) made offshore relatively uneconomical. On the demand side, the ESG narrative started to dominate headlines and investors flocked to sectors like renewables and electric vehicles, expecting oil demand to peak within a few years. Given the long duration nature of offshore oil, it no longer made sense to commit capital for 5- 10 years towards new offshore projects.

The demand shock experienced by these factors was exacerbated by the supply side / new-build environment. Several years of high dayrates and strong customer demand had incentivized offshore drillers to invest heavily in new rigs, with new builds running as high as ~30% of the existing fleet size during the peak boom years in 2009 - 2013. During this period, the offshore drillers invested the majority of their cash flow into new assets, just as demand was about to fall off a cliff. Rig orders were aggressive, primarily in Brazil, GoM, West Africa and the North Sea.

The negative shocks on both the supply and demand side created a perfect storm for the industry. The offshore drilling business is highly leveraged, both operationally (mostly fixed costs) and financially (most driller take on large quantities of debt to finance new builds), which meant that the conditions that developed post-2015 drove most of the major companies into bankruptcy / restructuring. As E&Ps cut contracts, 4 out of the 7 largest drilling companies (Valaris, Noble, Seadrill, Diamond) sought creditor protection. New build construction collapsed and many of the major shipyards suffered heavy losses.

After a 6+ year brutal bear market that destroyed billions in capital, the prospects for the offshore industry are improving again:

US shale production is peaking and becoming gassier, forcing E&Ps to look at offshore again for the best quality oil and exploration prospects.

With ESG / peak oil demand narratives proving false, oil producers are becoming more open to investing in long-cycle projects.

The offshore new-build industry has been decimated. A number of the major shipyards in Asia (China, Korea) have permanently shut down, and the skilled labor required to build offshore rigs have moved on to other industries.

Even if new build orders were possible, offshore management teams have no interest in spending on capex, after overinvesting and being left for dead by their E&P customers in the last cycle; the focus is on maximizing cash flow, deleveraging / returning capital to shareholders.

~80% of offshore reserve breakevens have dropped to <$65 / bbl. With multi-year underinvestment in upstream capex and OPEC+ having more market power, sustained >$65 / bbl oil is more likely in the coming years.

Even for OPEC countries like Saudi Arabia and UAE, offshore investment is picking up significantly as mature, onshore assets deplete.

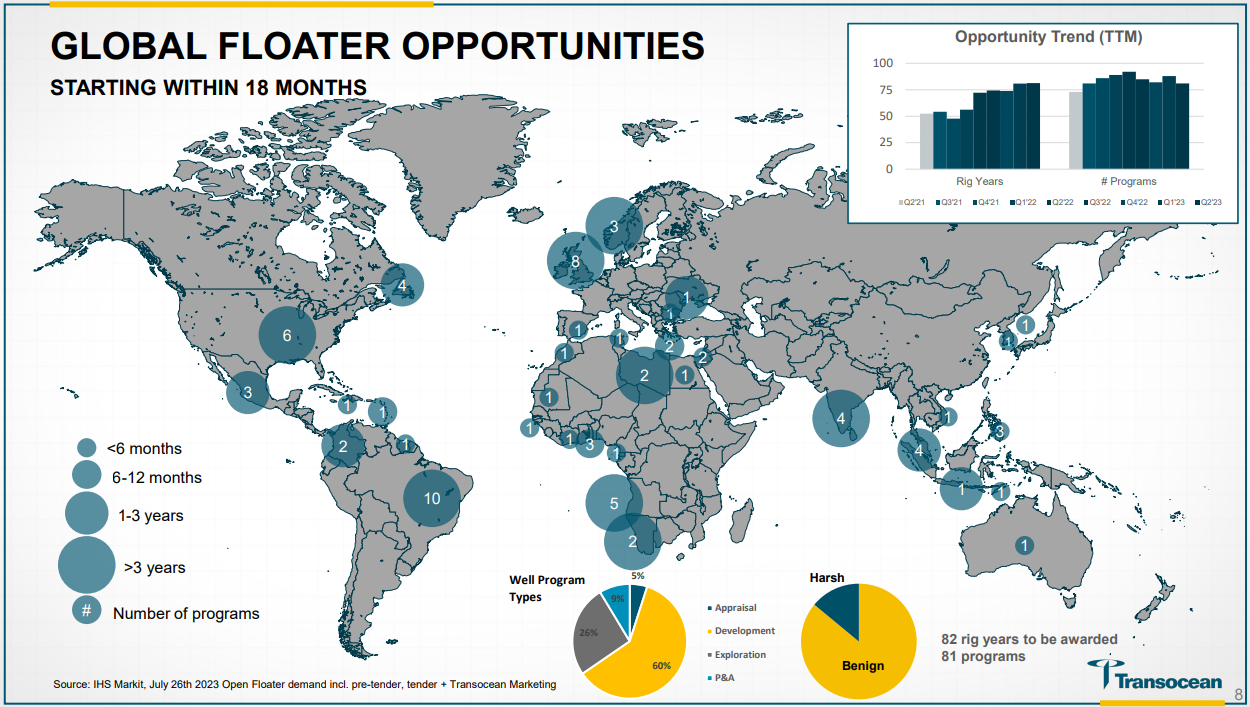

As a result of the above dynamics, the supply / demand picture has flipped with demand now expected to outstrip supply for several years. Dayrates and utilization have started inflecting upwards, especially for the deep water and ultra deep water (UDW) segments which tend to be the most cyclically sensitive. UDW dayrates have more than quadrupled after bottoming out at ~$100K in 2018/19 to now >$400K. Utilization rates for drillships have reached 90%+, a level last seen in 2014.

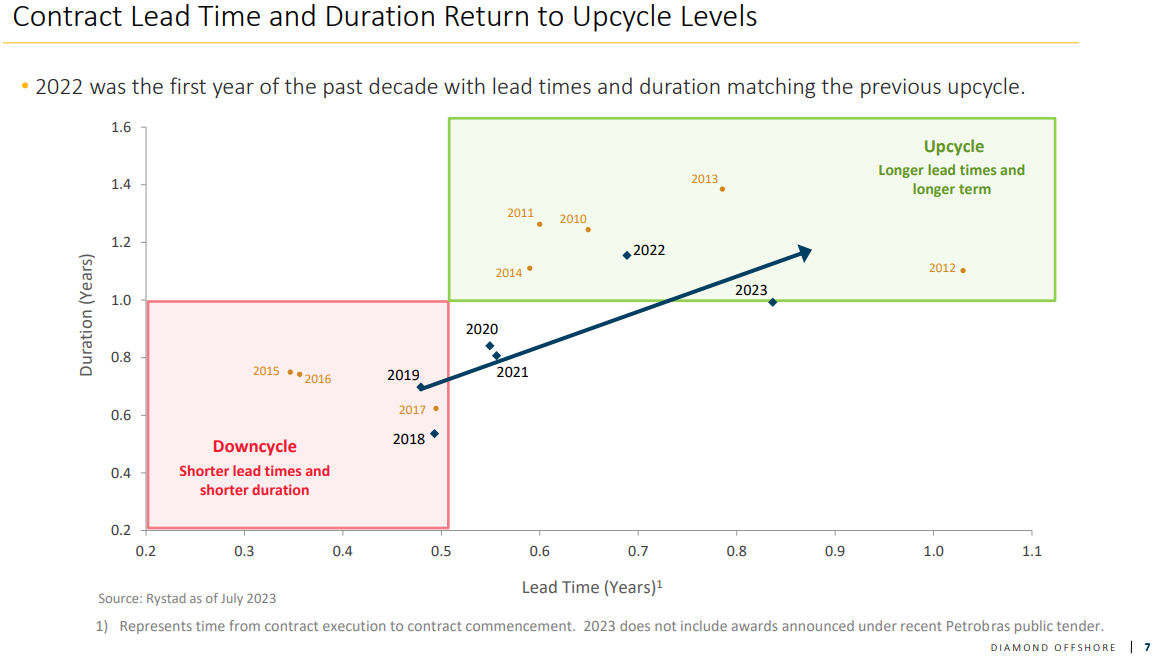

Contract durations and lead times (from contract execution to contract commencement) have also been lengthening and reverting back to 2010 - 2014 upcycle levels. For example in 2018 - 2021, E&Ps typically signed offshore contracts 6 months in advance and the contract length was typically also 6 months. Most recently, in 2023, contracts on average are being signed 9-10 months in advance and for a duration of 1 year. This reflects that E&Ps are cognizant that offshore drilling services are in short supply and want to lock in services and rates sooner, and for longer periods.

2024 planned offshore capex of $162bn is the highest since 2017. As I mentioned previously, E&Ps are turning to offshore and deep water because U.S. shale opportunities are now limited, with all the prime acreage taken up (two of the three major US shale basins, Eagle Ford and Bakken, have already peaked and are in terminal decline). National oil companies (NOCs) including those in Saudi Arabia, Abu Dhabi and Kuwait are also currently expanding offshore production.

After the big offshore development in Brazil / Guyana (expected to produce >1mm b/d in 2027), Namibia, Suriname, South Africa, Eastern Mediterranean, Tanzania and Columbia are all in contention for the next big offshore projects, with promising early drilling results or seismic data. Namibia in particular is a popular destination for offshore exploration right now, with 4-5 major oil producers drilling wells there already and potential production expected to exceed even Guyana.

In July this year, Sclumberger had the following to say about the offshore market (emphasis mine):

“We see also the emergence of the second leg of FID and future offshore expansion driven by exploration appraisal. Exploration appraisal is happening in many countries. There are many rounds of licensing rounds happening, a lot of exploration and appraisal is happening to find this next reserve and develop it. So offshore is there to stay and not only in 2024 or 2025, but beyond as we can see, and with the second leg materializing.”

At this point, the following thought has probably crossed your mind already: how can one trust that the industry won’t misallocate capital to newbuilds and repeat what happened in the past cycle? After all, in a cyclical industry one has to expect the same types of behavior to be repeated in every cycle. To answer this question, I would encourage you to read the recent earnings and investor day transcripts of the major offshore players.

Below are some excerpts from the Q&A session at the recent Barclays Energy Conference.

Seadrill CEO:

“...every time I try to speak to a shipyard, they hang up on me…this is a distraction and abstraction…no one knows what it costs and no one is going to build one…maybe $1 billion and 3-4 years to build one…we have a baseball bat at the office and we use it to hit people if they say newbuild…we need $1 million a day or $1.2 million dayrates on a terminal to justify one…”

TechnipFMC (UK-based oil and gas services company):

“We’re seeing increasing demand for longer duration contracts and a focus on securing capacity…no one is building a new rig...maybe ever in our lifetimes..."

Valaris:

“We have zero expectation of a newbuild cycle. We will probably never see it happen. Newbuild parity is $900K for 10-15 years”

Noble:

“Newbuild parity is $650K for 15 years”

If you’re wondering what these CEOs mean by “newbuild parity” - they are referring to the level of dayrates required for the company to justify investing in a new vessel. For example, Valaris is saying that dayrates of $900K would be needed for 10-15 years before they consider investing in a new ship. If this is true, then the offshore industry will remain in a supply-constrained environment for a very long time. Dayrates would eventually need to converge to newbuild economics to bring more supply on, and it would take another 3-5 years to build these ships.

Is it possible that all these CEOs are just saying what they need to say to attract investors? The fact that everyone in the industry, including the shipyards, have no idea what it’s going to cost to build a new drillship, and are not even interested in having the discussion at this moment, suggests to me that we are still pretty early in this cycle. As part of my due diligence, I reached out to someone who is a captain on an offshore drilling rig and he confirmed that everyone in the industry is still extremely scarred from the last downcycle; his company management feel that they still haven’t been adequately compensated for the drillships they invested in during the last cycle, so investing in new vessels this cycle is the last thing on their mind.

Even if we assume that everyone is lying, and the CEOs decided to invest in newbuilds at this stage, the drillers would still need to somehow convince the shipyards that this time is different (most of them went bankrupt in the last cycle) and get them to mobilize and train / retrain hundreds of thousands of people who lost their jobs during the downturn. The drillers would also need to offer much higher initial deposits (deposits were 10% during the boom, with the rest financed by the yard and export banks, but the shipyards are now demanding 50-60% upfront).

Transocean (NYSE: RIG)

To play this thesis, I’ve decided on a barbell strategy by taking a position in the most leveraged / torqued player (Transocean/ NYSE: RIG) as well as the largest, cleanest balance sheet in the industry (Valaris/ NYSE: VAL). I’ll be covering Valaris in more depth later on.

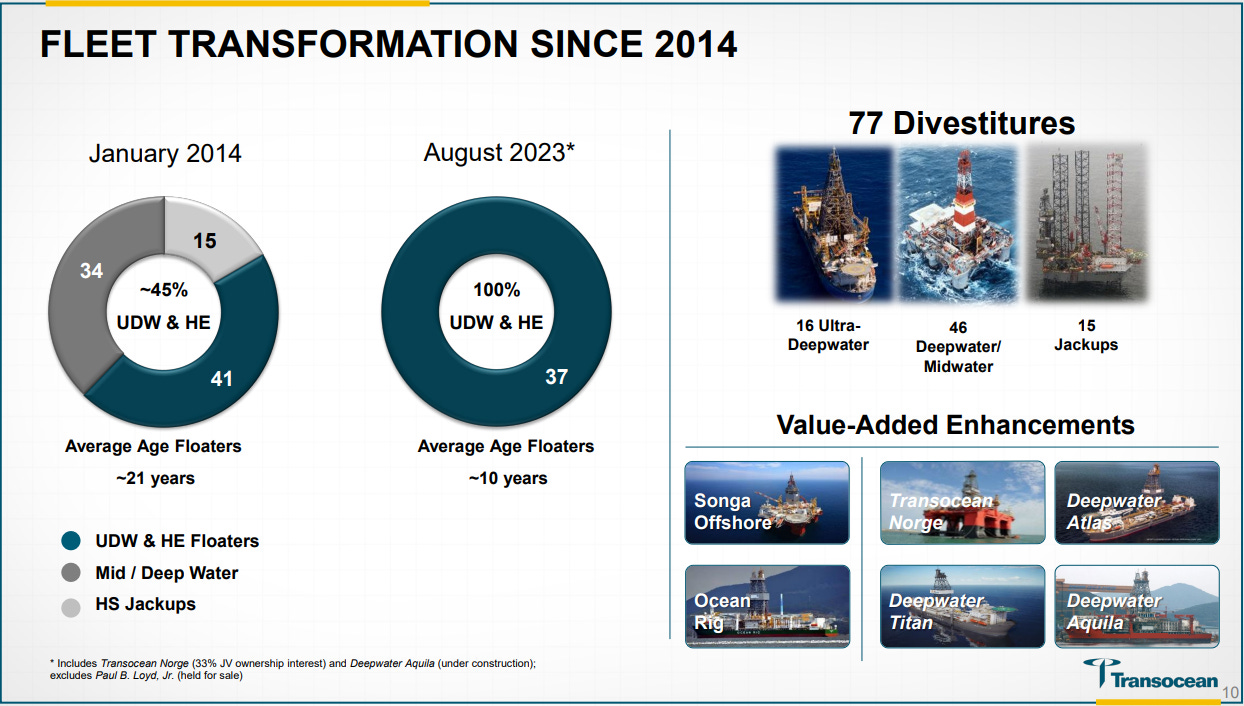

Transocean is one of the few companies that survived the offshore downcycle without going into bankruptcy. As a result, the company is highly leveraged with Debt / 2023e EBITDA of ~8x. While that’s a scary number, therein lies the opportunity.

During the downcycle, RIG significantly reduced the size of its fleet through scrapping and divestment of non-core assets, adding modern drillships and narrowing its focus on ultra deepwater (UDW) and harsh environment (HE) floaters. The company currently owns 37 vessels with an average age of about 10 years (industry average is 20+ years), excluding one being sold. RIG has 28 UDW vessels, and 9 HE vessels in its fleet. 26 of its vessels are operating, 11 are cold-stacked, and one is under construction. With dayrates inflecting sharply upward, RIG now stands to benefit disproportionately as UDW and HE floaters are the most cyclically sensitive in terms of dayrates. Having 11 cold-stacked vessels offers optionality to take advantage of higher dayrates in the future.

For Q2, RIG saw its average dayrate climb 16% YoY to $363K, up from $312K. More importantly, RIG guided to a Q2 2024 average day rate of $433K, which would be a further 19% increase from today’s level. The CEO had the following to say about the current market outlook (emphasis mine):

“Not only have we increased average day rates for our ultra-deepwater fleet, we've also experienced a rapid tightening of the high-specification harsh environment semisubmersible market. As recently confirmed by Westwood Global Energy Group, this asset class is now effectively sold out with committed utilization at 100% for the first time since 2014. We first highlighted the emergence of new harsh environment regions on our third quarter 2022 earnings call. At that time, we predicted that the exodus of high-specification semisubmersibles from Norway would lead the Norwegian market undersupplied in 2024. Even so, we underestimated the speed and magnitude of this migration. Since then, 3 of our rigs, the Transocean Barents, the Transocean Equinox and the Transocean Endurance have moved or are preparing to move to new markets, including Australia and Lebanon. And we see more movement on the horizon as opportunities for these assets continue to develop, deepening our conviction that this market will remain tight for the foreseeable future. Compounding these supply constraints, expected demand for the Norwegian market may be nearly 20 rigs by 2025. If this work materializes, Norway will be significantly short of supply as only 12 high-specification harsh environment semisubmersibles are anticipated to remain in country through this period. As a natural consequence, day rates for harsh environment semisubmersibles have meaningfully increased since the beginning of the year and are now rapidly approaching $500,000 per day for firm work with certain price options already above this threshold.”

At a $433K dayrate by Q2 2024, RIG should annualize roughly $1.5bn in EBITDA per my calculations, vs. 2023e EBITDA guidance of $840mm. If day rates climb to $500K as RIG CEO and Wood McKenzie suggest, RIG should annualize $2bn in EBITDA. With $300mm in maintenance capex, this would generate ~$1.3bn in FCF (assuming debt paydown throughout the year and exchangeable bonds early converted), increasing to $1.7bn as the company deleverages, on a current market cap of ~$7.8bn. If RIG decides to re-activate its 11 cold-stacked vessels, that would generate another ~$500mm of EBITDA, but would require some upfront capex.

While RIG shares are up 80% this year, shareholders can still earn a significant return if the offshore thesis plays out. Current net debt is $5.5bn, assuming the company’s exchangeable bonds are fully converted. Given all the exchangeable bonds are in-the-money, and the fact that the company has received numerous queries about early conversion, I think that’s a reasonable assumption. Fully diluted shares upon conversion would be 945mm (766.7mm shares outstanding + 22mm in outstanding share-based awards + 9mm warrants + 147.2mm shares underlying the exchangeables). This would imply $5.8 per share in equity value creation from de-leveraging over ~4 years (with a flat $500K day rate assumption), or +71% from today’s share price.

A 71% return over 4 years might seem quite modest for a highly leveraged stock in a cyclical industry, however I would like to point out that the above math is quite conservative:

Re-activation of cold-stacked rigs would further improve EBITDA and cash flow.

Dayrates reached ~$600K during the last upcycle.

If we inflation-adjust the prior cycle day rates and also take into account newbuild /parity economics referenced at the recent Barclays conference, one can justify dayrates in the $700K - $1mm range.

In addition, if one assumes multiple re-rating, the potential upside could be much higher. During the last upcycle RIG traded at an 11 - 13x EBITDA multiple range (see chart below). Assuming $2bn run-rate EBITDA, this would result in a $23 - $28 share price once the company is fully de-leveraged.

If that price range sounds absurd, we can triangulate value another way: looking at replacement cost. RIG owns very high quality, scarce assets that are in high demand and extremely difficult to replicate. One can argue that the equity should reflect the fair value of these assets.

The current book value of PP&E (net depreciation) is $16.9bn, or roughly $460mm per vessel. Based on RIG’s current market cap and EV of $7.8bn and $13.3bn respectively, the market is valuing the vessels at ~$360mm per vessel.

However, we know from RIG CEO’s recent comments that new builds are ~$1bn in cost.

RIG’s recently ordered Atlas and Titan vessels cost $2.25bn or $1.1bn per unit, however these are state-of-the-art, 8th generation ships. 7th generation ships are roughly $850mm - $1bn in value and 6th generation, a bit less.

If we value the company’s 37 vessels at a conservative $500mm per unit, the current net asset value per share is $14 and $20 pre and post deleveraging. At $1bn per unit, those numbers would be $33 and $39, respectively.

In other words, while a 11-13x EBITDA multiple might seem egregious, it would essentially value RIG at replacement cost, while also being in line with historical upcycle multiple range.

Bringing these data points and train of thought together, I view RIG upside as 2 - 4x from here over the next 3-5 years, depending on the length of the offshore upcycle, and investor enthusiasm for the sector as the thesis matures.

One final point on valuation: during the last upcycle, RIG traded at a 50 - 100% EV premium to book value of assets. This would imply an EV of $26 - $34bn and a stock price of $21 - $30 pre de-leveraging, and $28 - 36 post de-leveraging.

Risks to the thesis and some timing considerations

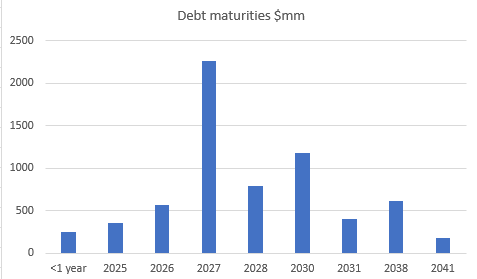

Given the high level of operational and financial leverage at RIG, the big risk to the thesis is that dayrates don’t inflect upward and that RIG is unable to generate the cash flows needed to support the current enterprise value and debt (interest expense alone is $500mm+ / year on the current debt stack). The company has sufficient liquidity ($821mm cash) to meet its debt maturities for the next couple of years. However there is a big debt wall in 2027 that would require healthy cash flows and market environment to be refinanced / repaid. It’s important to remember that the company was free cash flow negative as recently at Q2 of this year, and the de-leveraging story is yet to even begin.

What could cause dayrates to stagnate or fall from here? If I’m wrong about the oil thesis and if oil falls and stays below $65-70 / bbl, then offshore will no longer be as attractive for E&Ps. Alternatively, there could be a temporary crash in oil prices due to a recession, or a financial crisis, which could cause a large draw down across the energy sector stocks.

While the offshore thesis will work if oil averages >$65-70 / bbl, the offshore stocks could remain correlated to oil price in the short run. The inflection upwards in dayrates will be gradual and I don’t expect a sudden jump to $600K+ dayrates. The first step of the process is for cold stacked rigs to come back online. Once idled rigs are fully contracted and supply is exhausted (next 1-2 years), that’s when dayrates are likely to start spiking to newbuild parity. That’s also when investors are more likely to start valuing these companies on replacement cost / asset values to achieve the upper end of the valuation ranges I posted above. In other words, to earn a multi-bagger return you’ll have to be patient and stomach lots of volatility in the interim.