It's Not Supposed To Be Easy

The mental aspect of holding through drawdowns, why Kazatomprom's (KAP) guidance is not bearish, uranium price signals, Cameco's earnings call

"It's not supposed to be easy. Anyone who finds it easy is stupid." Charlie Munger

The volatility in my core holdings this week has been challenging to deal with mentally. It’s tough seeing your portfolio drop precipitously for days, when you’re confident in the underlying fundamental thesis for your investments. But it’s also the price of admission in public markets investing. During times like these, I remind myself that it’s not supposed to be easy, and that you earn your stripes as an investor during periods of heightened volatility. Can you stick to your guns when the market is screaming at you that you’re wrong? Can you stay calm when others are panicking? Can you buy / add to your positions when every part of you just wants to turn off the screen and walk away in disgust?

If doing all of this was easy, then anyone could do it. At the end of the day, the market owes you nothing. The stocks you own don’t care about your analysis. To generate alpha you need to have an out-of-consensus view, and be right on that view, which is a hard thing to do given the number of smart people all trying to beat the market. On top of that, even when you’re right, your profits will rarely come when you expect them / want them. In the interim, price action will test your conviction.

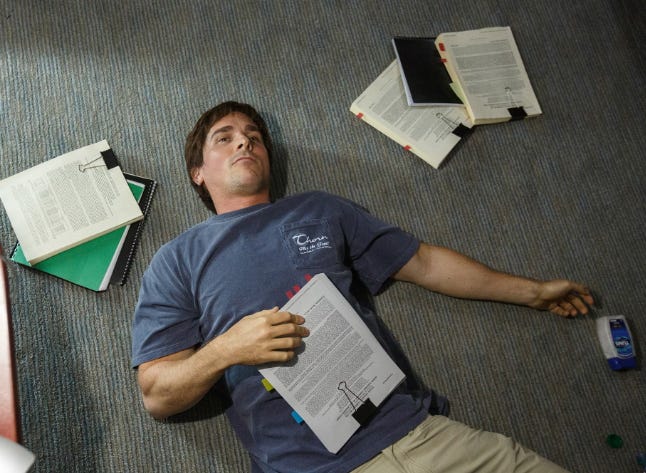

Markets are great at sniffing out where the pain points are, and flushing out the weak hands, such as folks who buy a stock without having done their own research (“lazy longs”), or folks who are over leveraged. One of my really smart friends likes to say: “you can’t borrow someone’s conviction”. Sometimes, prices can go to such extremes that even the best investors start doubting their ideas. I’m reminded of the scene in the Big Short where Michael Burry is lying on his office floor in frustration, mentally exhausted from checking and re-checking his analysis a gazillion times, while the market kept going against him.

Since May, my positions in the uranium sector have gone down in almost a straight line. In terms of magnitude, this sell off (peak to trough) is now significantly worse than even the 2023 SVB crash. On Thursday and Friday this week, my portfolio experienced the worst single day losses of the year. While all of this is happening, my research continues to suggest that fundamentals for uranium are trending in the opposite direction. As maddening as it may sound, the future prospects for nuclear power look brighter each day, and supply growth looks more and more uncertain.

That’s not to say that I got everything right. Below are some blind spots I missed over the course of this year:

I believed KAP’s lowered production guidance, and the ban on Russian uranium, would lead to a squeeze higher in uranium price in the first half of this year. However, US utilities were able to purchase enough spot material and flex up existing contracts to be sufficiently covered over the next 2 years. While 2 years is the bare minimum inventory coverage, it means utilities are not in a ‘panic mode’ today, allowing them to step back from the market as they figure out the waiver process.

I had expected KAP’s production to be in line with or below guidance this year, but KAP was able to grow its production more than anticipated in the first half of the year, increasing 2024 production guidance from 21-22.5mm tU to now 22.5-23.5tU. It is also likely that 2025 production guidance will be revised upwards.

I was too sanguine on the prospects of a spot market rally and didn’t account for price insensitive selling from sources like the Japanese utilities (Hokkaido). While the spot market is only 20% of the total uranium market, it’s the most visible uranium price level, and investor sentiment has not been helped by a sideways chop in the spot price.

The important point though is that being wrong on these market dynamics doesn’t invalidate the bull thesis for uranium. The fact that US utilities are covered, doesn’t solve the 30-40mm lbs primary deficit. A deficit implies that someone, somewhere has to draw on inventories to meet consumption needs, and as inventories dwindle, price has to rise. When utilities exercise flex up provisions, producers like Cameco and KAP have to figure out how to procure the lbs necessary to fulfill the higher supply commitments. Last year, they were able to do this by selling out of inventory, buying in the spot market, borrowing lbs, and/or exercising purchase contracts. As a result, KAP’s inventories fell to an eight-year low and spot price rallied from the $50s to >$100 / lb. The situation hasn’t changed this year. This is why, despite the recent sell off in the equities, uranium prices are still 2x where they were in 2022. As long as the deficit persists, prices will continue to be pressured higher, though clearly not in a straight line.

What about the KAP production increase? Will KAP flood the market with uranium and shift balances into a surplus? A 2-3mm lbs production increase is not meaningful relative to the size of the deficit, especially keeping in mind how quickly the future demand picture is improving. Based on the current demand projections, there is 2.1bn lbs of uncovered uranium demand to 2040. This cannot, and will not be satisfied by KAP alone. Readers who have been following my analysis of KAP will remember that KAP’s initial 2024 guidance was 24.5K tU. Despite the recent increase, production is still tracking 6% lower than that level at the mid-point. 2025 guidance remains at 31K tU, and will likely be downgraded later this month (though will likely show a modest growth from 2024 production level).

We also know that KAP’s mineral extraction tax (MET) rate is going up by 50% next year. It is entirely possible that KAP is prioritizing its acid usage this year to boost production and replenish inventories, as increasing production next year will be more penalizing from a tax perspective. KAP’s inventories were down by more than 20% YoY at the end of 2023, and the Company owed 3.7mm lbs to ANU Energy and Yellowcake in the first half of 2024. Note that KAP’s increased production guidance did not lead to a change in its sales guidance.

Investors should also pay attention to where the production increase is coming from within KAP’s asset base, and put this in the context of geopolitical bifurcation. Cameco’s recent earnings call highlighted the fact that JV Inkai production decreased ~20% YoY. Semizbay and Ortalyk (Chinese JV) have also produced slightly below estimates in H1 2024. So KAP’s production increase must be coming from its crown jewel asset, Budenovskoye 6 & 7, which is a JV with Russia. This implies that KAP’s production increases beyond inventory replenishment will likely go to the Russians, and will not help secure any fuel supplies for Western utilities.

In summary, I don’t believe that a slight increase in KAP’s production guidance this year indicates that its sulfuric acid problems are resolved. While we might see another marginal increase in production for 2025, it won’t be meaningful to the deficit. The Company will struggle to grow supplies significantly until its new sulfuric acid plant comes online (likely 2026+), and by that time demand will be 10-20mm lbs higher.

If I’m wrong in my analysis, and traders are genuinely worried that KAP will eventually push the market into a glut, then one should expect fuel prices weaken substantially. Instead, while uranium equities have been crashing, uranium spot price has found support in the low-$80s, a level that has held since March of this year, and is now converging with the LT price. Multiple times now, Chinese buyers have shown up to purchase pounds when spot prices dropped to this level, creating a floor price. The Chinese are very close to Kazakhstan, and are intimately familiar with KAP’s operations. Would they be so eager to buy in the low-$80s if they knew a flood of KAP supply was about to come online?

In the month of July, spot UF6 prices increased $5, from $281/kgU to $286/kgU. Spot conversion price increased $7 to mark a new all-time-high price of $67. Spot SWU prices were unchanged, but LT SWU price increased $4, from $159/SWU to $163/SWU, representing a 14-year high. LT U3O8 price closed at $80.50 for July, marking a 16-year high. These are the not the kind of price moves you see in a market that is on the brink of oversupply.

LT U3O8 contract prices are an important indicator of the health of the market as 80% of uranium purchasing happens through LT contracting. It’s also important to remember that LT contract price reporting underestimates the current pricing environment, as it only represents the lowest offer base escalated price. Sometimes, there is no uranium transacted at that price. Imagine a scenario where your neighbor’s house is sold for $500K. A day later a buyer shows up and offers $350K for your house. You would obviously never accept this offer given the recent comparable transaction at 40% higher price. However, based on how uranium LT contract price reporting works today, the price reporter would report a price level of $350K for houses in your neighborhood.

For a more accurate gauge of the current LT contracting environment and sentiment, see the comments below from Cameco during this week’s earnings call:

“With a stronger market environment, we’re currently locking in ceilings of about $125-130/lb, and floors at about $70-75/lb in market-related contracts, the best prices seen in over a decade.”

"The days of easy and cheap pounds out of central Asia are essentially over. The global cost curve is going up and we are going to need to see sustained higher prices."

“We see a very constructive setup occurring. And once these factors [referring to the Russian ban / waiver situation] have cleared and there's a bit more certainty, we do expect to see the type of demand approach replacement rate. And of course, if it goes beyond, that will be a very, very constructive time in the market because we've never been at these prices at a below replacement rate scenario before. So I would say the opportunity for upside appears to be much, much greater than the opportunity for downside.”

In other words, we’re seeing a very strong contracting market this year, despite contracting volumes nowhere near replacement rate. It’s not hard to imagine what would happen to prices if utilities decided to contract >100% of their annual consumption, as they have done in past bull markets. The quote below from Brandon Munro, Managing Director at Bannerman Energy (ASX: BMN), further crystallizes this dynamic [emphasis mine]:

“The amount of contracting and spot market purchasing by end users in this sector has still not reached what we call replacement level contracting. So for anyone who's out there who's been following the sector and looking at it carefully for some time and is frustrated that there isn't more action, well, I would put to you that it's remarkable that we are still in a trading range of the mid $80’s per pound on the spot market with a long term contract price that roughly reflects that, even though the sector is not yet expressing itself in economics for the deficit. So in other words, the deficit is not being exposed because the utilities are not buying enough uranium to restock what they're using and therefore not buying enough uranium to expose that deficit.

So as an overall market for uranium, I think the key principles are it's very, very strong as evidenced by the current price. The downside/upside risk remains in asymmetry. We've seen even with uranium coming under some spot market pressure in recent weeks, key players including consumers of uranium have been happy to step in and start mopping up pounds.

So I feel like we're pretty close to a foundational base or a floor in uranium where it is now. And we've got a number of tremendous demand pressures that are building up over the next six months in particular. The first demand pressure is simply that utilities start to contract again and start replacement level contracting.

The second, and we can come on to this if you like, is what happens when it moves from replacement level contracting to instead of destocking, they change into restocking. And then what happens when all of the key demand signals and the demand growth that's in this sector start to have an impact on this market. So I feel very, very confident and very comfortable with where we are in the sector.”

The recent uranium market crash seems absurd in light of these facts. I’ve spoken to a few fellow investors on this topic, and based on the intel I’ve gathered, below is my best guess for why the recent draw down has been so violent:

A number of hedge funds have been chasing the AI theme and started buying uranium stocks as a ‘picks and shovels’ play on AI. With the AI hype cycle cooling off, uranium stocks were dumped in haste given they were a non-core holding, and their illiquid / volatile properties made them toxic to risk management models during draw downs.

This dynamic was exacerbated by a VaR shock resulting from the unwinding of a couple of massive hedge fund trades:

The short Yen / carry trade (borrowing in Yen and then buying US stocks) has been extremely popular with hedge funds, and with the Yen suddenly strengthening from 157 to 146, we are seeing a cascade of de-leveraging and losses.

Poor economic data out of the US is creating a panic that the Fed may have been behind the curve on easing, and that a recession is now inevitable.

The overall commodity complex has suffered a sharp drawdown in July, with heavily traded commodities like oil and copper suffering from 15-20% drawdown.

While uranium is a non-cyclical commodity, it tends to come along for the ride during such periods of broad commodity and equity weakness.

July and August have historically been weak periods for uranium as fuel buyers are on vacation, and the spot and contracting markets are usually quiet. I’ve explained in the past how the uranium buying process is quite distinct from other commodities, and buyers are unlikely to show any sense of urgency relative to their typical buying procedures / timelines, regardless of what the market does.

The last thought I want to leave you with is that the situation in the uranium market is the result of a decade of low prices, underinvestment, and a consensus view that the nuclear sector would remain in terminal decline, in favor of renewables and other green technologies. The original thesis was never predicated on AI demand, or geopolitical bifurcation, or the banning of Russian uranium. It was simply a recognition that if the consensus is wrong, and if nuclear power is here to stay, then the investment needed for supply to catch up with demand won’t come on time, leading to higher uranium prices. So when investors are losing their minds and dumping uranium stocks because KAP will increase production by 5%, or AI may not be worth the hype, or US utilities may get waivers from the Russian ban, in my humble opinion they’re not thinking clearly. I’m putting my money where my mouth is and have added to my positions.

Thanks for the pep talk. I have no doubt spot price will go up. You have educated me with all your articles (lots of homework for me). It is a pleasure to read your artices. I don't want to put you on a pedestal but that's damm fine work. And to communicate it all in words is amazing. Thanks, Chris

Im holding on to spot.