Iran Trade

Planning for a drawn out conflict

While Wall Street and sell-side analysts are busy trying to downplay the conflict in Iran, I’m increasingly concerned that this will be protracted, and more harmful to growth than the markets are currently pricing in. I’ve de‑grossed my portfolio this week to my highest‑conviction trades and entered a couple of new positions I think will perform well in a prolonged conflict scenario.

If I’m wrong and the conflict ends quickly, markets will rally and my holdings will rise with the tide. If I’m right, these trades will act as needed portfolio insurance against broader equity weakness.

In recent days, several analysts have taken comfort from US government statements that Iran is being hit hard, that it will soon run out of missiles, and that the situation will be under control in a few weeks. Iran also signaled a willingness to talk, leading some to speculate the US/Israel campaign is working and remaining IRGC forces will succumb to pressure.

Trump’s announcement that commercial vessels transiting the Strait of Hormuz will be escorted by the US Navy, and that the DFC will provide an insurance backstop, helped stabilize oil prices. The market is also expecting a Strategic Petroleum Reserve (SPR) release to calm energy markets further.

While these developments may have alleviated near-term market shocks, I believe they don’t capture the full spectrum of risks:

It’s clear that the magnitude of Iran’s initial response overwhelmed the US, Israel and the Gulf states.

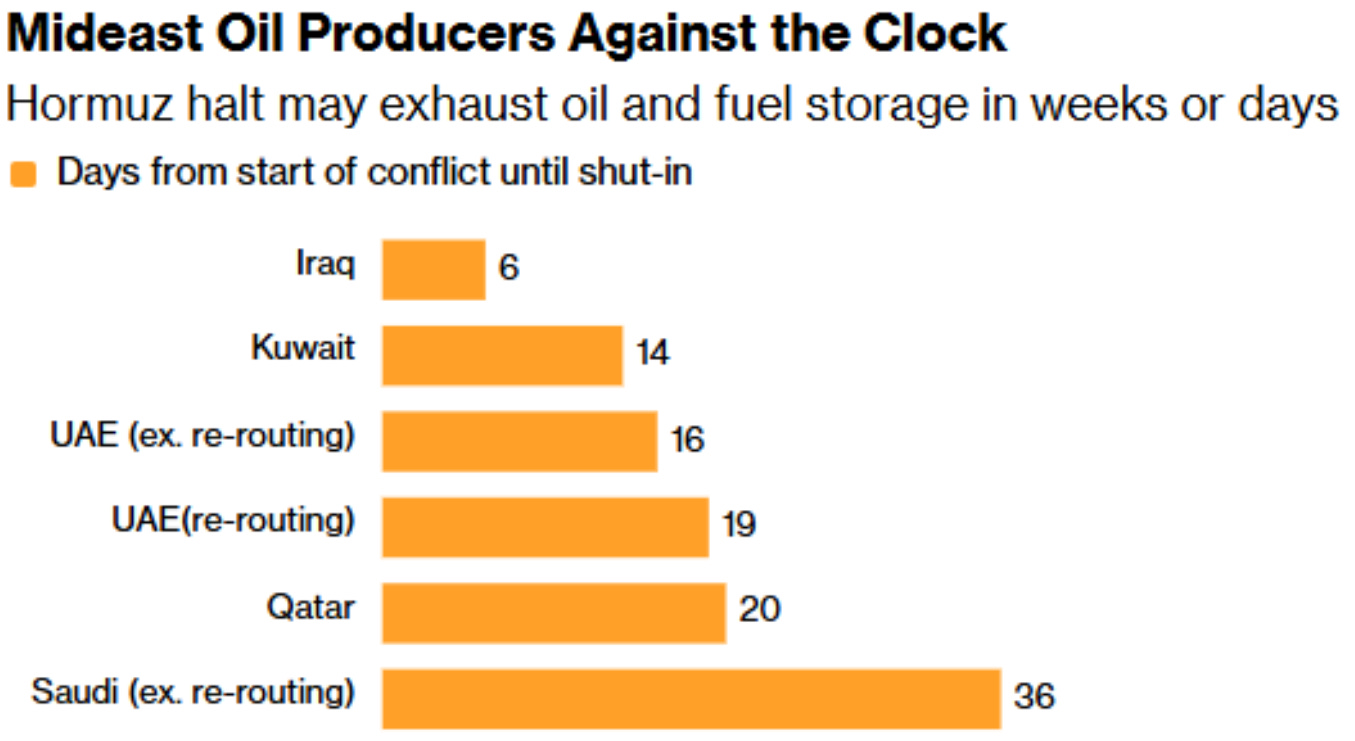

Critical energy infrastructure has been damaged: Iraq has been forced to cut oil production and Qatar has declared force majeure on LNG contracts. Saudi Arabia and the UAE could be next. Oil and fuel storage could exhaust quickly.

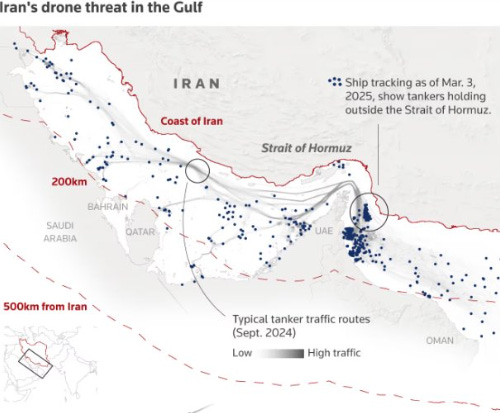

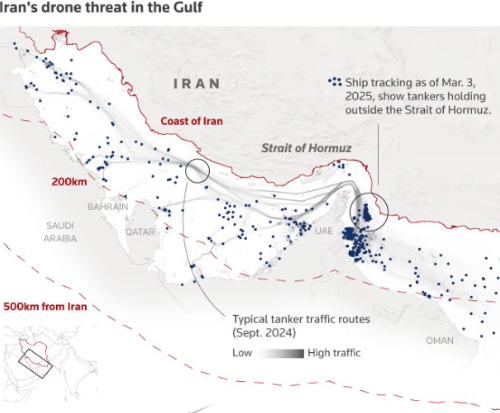

Strait of Hormuz volumes have dropped more than 90%. Goldman Sachs currently expects volumes to normalize by April, but geopolitical analysts warn that Iran could disrupt the Strait for months.

Hormuz not only accounts for 20% of global oil supply, but also 30% of global chemicals supply (fertilizers, LNG, processed fuels etc.). If volumes remain at current level for more than a month, oil prices could spike to triple digits.

All twelve protection and indemnity (P&I) clubs of the International Group, which cover ~90% of the world’s ocean-going tonnage, have issued cancellation notices.

Trump ordered the DFC to provide political risk insurance, but several ship owners told Reuters they’re uncertain how it will be implemented, and whether the DFC as sufficient balance‑sheet capacity to cover the exposures.

The US has also offered to individually escort tankers through the Strait, however this will be enormously expensive and make US navy vessels more susceptible to attack.

The Houthi attacks in the Red Sea are the closest maritime analog. The attacks began November 2023 and 26 months later traffic remained 60% percent below pre-crisis levels.

The US tried escorting vessels then and eventually gave up.

Ships that wanted to avoid the Red Sea could take the longer route around South Africa; however in the current scenario there are few other paths to exporting oil and petrochemical products from the Persian Gulf.

Iranian forces are significantly better equipped and more sophisticated than the Houthis.

Commodity data and analytics provider Kpler estimates that the path back to normalcy will be measured in quarters, not weeks.

Several US bases have been hit and expensive equipment destroyed.

Satellite imagery shows an Iranian ballistic missile struck the AN/FPS‑132 phased‑array radar at Al Udeid Air Base in Qatar, a ~$1.1bn asset that took years to build and provided critical early detection.

The strike demonstrates even sophisticated US defenses cannot guarantee protection in a high‑momentum attack environment and highlights the asymmetric nature of the conflict: Iran can use relatively inexpensive, quickly replenishable missiles to strike high‑value targets

Reports indicate the US and Gulf states are running low on interceptor stocks. Some Gulf states say they have used years worth of interceptors and that US resupply requests have been stonewalled.

It is unclear if the US has a governance plan for Iran in the aftermath of Khamenei’s elimination. Unlike Libya after Muammar al-Qaddafi, or Syria after Bashar al-Assad, where regimes collapsed as soon as the leaders were not in power, Iran has been planning for years to avoid their state’s future from being tied to one person.

Khamenei’s killing may further radicalize the region against the West.

Iran has ~90 million people and an army of ~1 million. If the state resists Western pressure despite leadership losses, there may be no quick solution.

Even if the Iranian State has been mortally wounded, it’s unclear who would govern the country going forward.

Regime change without boots on the ground is a risky proposition. Unintended consequences can emerge from the subsequent power vacuum.

The US is looking to support groups in Iran that are willing to take up arms to dislodge the regime. Kurdish militias appear to have started a ground operation.

History shows that such interventions are unlikely to remain confined to the region. Kurdish involvement could draw in Turkey and Shia militias from Iraq for example. The conflict will likely spread farther than is currently anticipated.

The macro implications of a prolonged conflict with Iran, and a destabilized Middle East, are quite clear. War is inflationary, and supply shocks are bad for global growth. This war also comes at a time when Western governments are running a fiscal dominance playbook with persistent budget deficits. War-time spending will make the fiscal situation worse.

A negative growth shock combined with higher inflation, which would make central banks reluctant to ease aggressively, will be bad for risk assets. Bonds are unlikely to act as a safe haven if inflation expectations are elevated. A stronger dollar will drain liquidity from the global capital markets.

A stronger dollar during an oil shock is particularly uncomfortable for Europe and Asia, because of the double whammy from imported inflation and tighter USD funding conditions. Tightening liquidity conditions abroad will likely spillover into US capital markets.

The Trade

In light of the above, I’ve increased my portfolio cash position from near zero to 5-10% by getting rid of most near-term call option trades and non-core ideas.

I’ve added a hedge:

Buy SPX 6800 / 6700 put spread, end of March expiration.

I like the following trade for oil (WTI):

Sell CL $65-$60 put spread for end of April.

The fair value of WTI absent geopolitical risks is in the low $60s. This trade expresses my view that oil price stays above fair value due to a sustained geopolitical risk premium, and takes advantage of elevated implied volatility.

I’m buying upside in US natural gas:

Buy UNG $12 calls for end of March and April.

Supply uncertainty in the Middle East will see global LNG prices stay well supported relative to where Henry Hub is trading.

TTF is currently close to $20/MMBtu vs. $3/MMBtu HH.

This means US LNG exports are likely to run at full capacity, making domestic US storage vulnerable to weather shocks.

At the current Henry Hub pricing, the market is not discounting any weather risk. If weather models turn colder for end of March and April, then US natural gas prices have 20-30%+ upside.

Last but not least, I’m buying some US chemical stocks:

Celanese ($CE): Two of the world’s largest low-cost methanol exporters, Iran and Qatar, have gone offline simultaneously. Methanol is the primary feedstock for acetic acid production via carbonylation.

As a vertically integrated acetic acid producer, Celanese will have a major cost advantage vs. competitors (who source their methanol from the spot market) from a prolonged methanol supply disruption.

Tronox ($TROX), Chemours ($CC): The titanium dioxide (TiO2) market is recovering from a long bear market. Chinese TiO2 makers use a sulphate process which is cheap, but uses a lot of sulfur. Almost 56% of Chinese sulfur imports come from the Middle East, all of which must pass through the Strait of Hormuz.

Sulfur prices in China have already surged 7%+.

US TiO2 makers like TROX and CC use a chloride process and will maintain a cost advantage as the global TiO2 market tightens.

Intervention - it’s war to the Iranian govt.

A while ago, CR & Trox were suggested by HFI Research, too.

Another account suggested (pointedly) that the GS estimate was too vague and offered further critique. Personally, fwiw, (like anyone cares) risk off for me.

"The fair value of WTI absent geopolitical risks is in the low $60s."

Why?

20% of supply is coming from the Permian which is depleting, Tier 1 wells are near to exhausted, if something that should be the bottom pricing. Demand can only go up but supply will hardly keep up