A Quick Note On Tungsten

Trump’s Iran strikes are likely to keep tungsten prices elevated given the demand shock from increased munitions usage, and the prospect of further Chinese supply restrictions as an indirect retaliation towards the US.

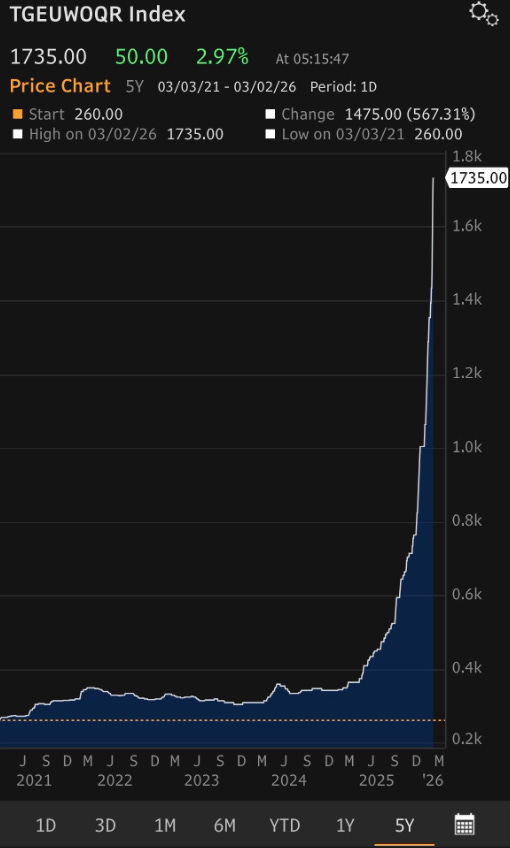

Based on the most recent price data, tungsten (APT) prices in China are close to breaching $2,000 / mtu, while Rotterdam is north of $1,700 / mtu. China’s 2026 mining quotas are being reduced a further 8%, marking a cumulative reduction of 14% relative to 2024 production levels. As of January 2026, Chinese exports are down 40% YoY.

According to metal.com, Japanese semiconductor companies have been notified that the delivery cycle for tungsten has been extended from 3 months to 9 months. European defense companies have initiated strategic inventory checks. A recently published S&P Global report states that even if construction started today, new tungsten mines would be unable to provide significant supply until at least 2030. It also points out that inventories outside of China are dwindling, estimated to cover only 3 months of demand, while domestic Chinese companies have begun to lock-in mine supply with 10-year long contracts.

With EQR up nearly 300% YTD, it’s tempting to want to take the money and run. But in light of the ongoing developments, which mark a perfect storm for the commodity, I believe there could be substantial upside remaining. These types of opportunities only come a handful of times in one’s investing career, and when they do, you have to stay in and go for the jugular.

In the short term, the slow pace of mine output resumption and Chinese export controls give marginal Western suppliers like EQR all the leverage. Since there is no substitute for tungsten, and tungsten usually makes up a small fraction of the total cost of the end products, the continuation of a parabolic rise is likely. How high prices go is anyone’s guess. In the medium-term the continued demand from high-end manufacturing, photvoltaics, semi conductors and military stockpiling should keep prices elevated.

I model EQR’s annual run-rate profitability at the current spot price under the following assumptions:

175,000 mtu production from Mt. Carbine.

125,000 mtu production from Saloro.

US$400 / mtu cash cost, 70-80% payability and 5% royalties.

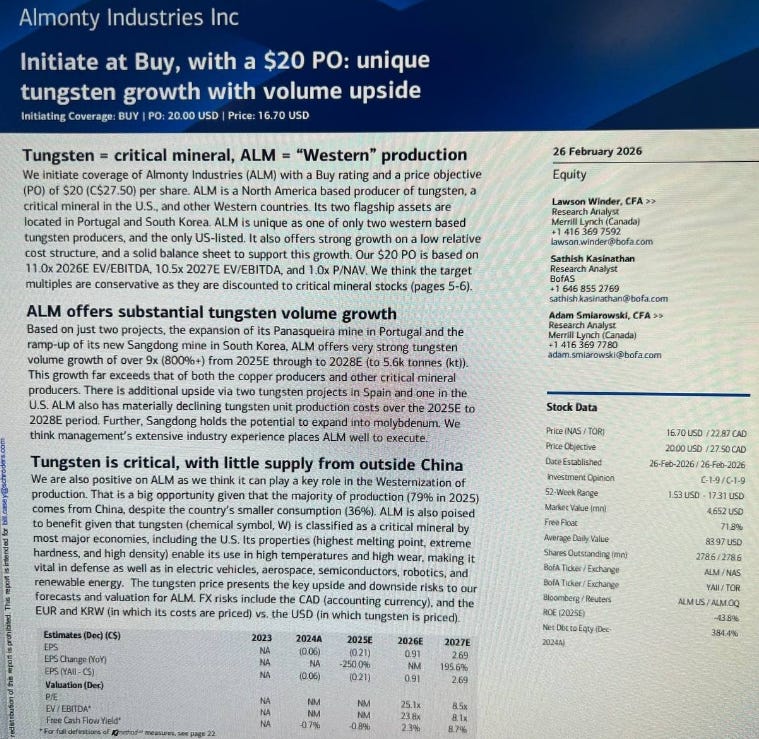

This results in an EBITDA of US$300mm. In a recent BofA research report, the sell side analysts ascribe a 10.5x EBITDA multiple to EQR’s peer, Almonty, citing comparable valuations of other critical mineral stocks. A 10.5x multiple implies a US$3.1bn valuation for EQR vs. the current EV of ~US$1.2bn. It’s worth noting that Almonty is currently trading at an EV north of US$5bn, with expected 2026 production of 125,000 mtu vs. 225,000 mtu for EQR.

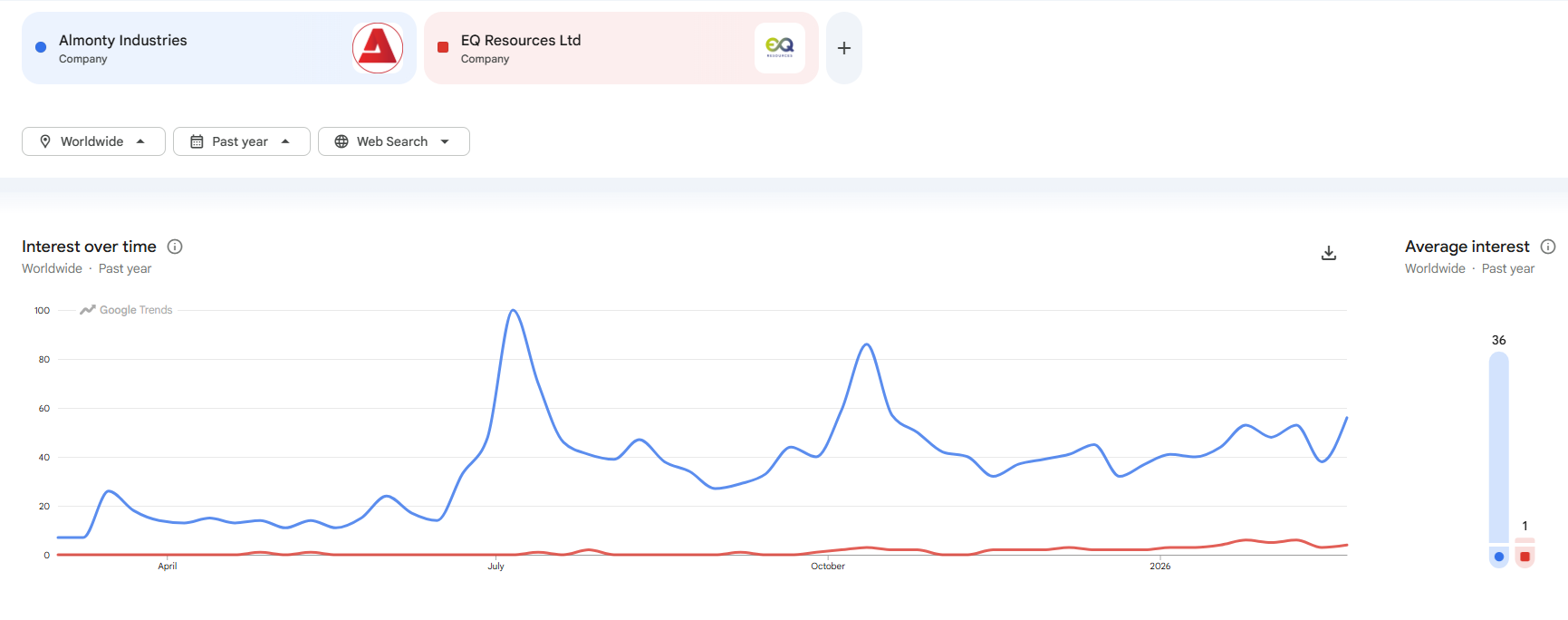

The biggest factor holding EQR back is that people simply don’t know about it. Even after the 300% price rise YTD, google search trends show that the stock is relatively unknown relative to its NASDAQ-listed peer. This is a massive opportunity for EQR management and investor relations team, but it also needs to be capitalized on quickly as no commodity bull market lasts forever.

There are multiple potential catalysts that could lead to a further re-rating in EQR and closing of the valuation gap vs. Almonty:

A continued rise in tungsten prices.

Inclusion in the ASX 300 (expected in March).

A strategic equity investment or takeover bid.

Upgrading production guidance now that the company has accessed the high-grade lolanthe vein.

I want to make it absolutely clear that valuing commodity stocks based on peak multiples and peak earnings is a recipe for losing money in the long-term. Tungsten, like every other commodity, will see a cyclical decline in prices once supply catches up. However, in the short-to-medium term, pricing dislocations can persist longer, and run farther than people imagine. The prevailing trend is for capital to rotate out of tech stocks into mining and commodity stocks, and critical minerals are likely to be continued beneficiaries.

I’m reminded of the following quote from George Soros that captures this idea well:

“I assume the markets are always wrong. Even if my assumption is occasionally wrong, I use it as a working hypothesis. It does not follow that one should always go against the prevailing trend. On the contrary, most of the time the trend prevails; only occasionally are the errors corrected. It is only on those occasions that one should go against the trend. This line of reasoning leads me to look for the flaw in every investment thesis. My sense of insecurity is satisfied when I know what the flaw is. It doesn’t make me discard the thesis. Rather, I can play it with greater confidence because I know what is wrong with it, while the market does not. I am ahead of the curve.”

Armed with the knowledge that the current valuation regime for mining stocks won’t last forever, and having already de-risked my cost-basis in EQR through scaling down, I’m staying long with the remainder of my position.

Thanks for the update. This is strictly a view from manufacturing: Tungsten, at these prices, will start to see a push back. There are some metals that are just too abrasive and Tungsten Carbide is necessary for cutting. However, there are a lot of other cases that Tungsten Carbide is preferred, but not necessary. There are some edge cases where it may make sense to do an entirely different (grinding, water jet, etc.) process than cutting.

McMaster Carr sells .375” diameter with .375” shank Carbide endmills for $43.49 each. McMaster Carr sells that same end mill, in Cobalt Steel, for $22.54. That price difference is enough that the shortened life of Cobalt Steel is tolerable.

The other end of pricing is Cubic Boron or TiSiN. Tungsten is moving up in price enough that the economics of Carbide becomes questionable versus CB or TiSiN tool inserts.

All metal cutting tools wear and eventually become unusable due to the very high temperatures at the cutting edge. Simply slowing the cutting speed down reduces tool wear. Using better (more expensive) coolant is also a way to prolong tool life. Both of these choices reduce productivity, but it is worth it when Carbide reaches a certain price point.

Well summarized mate, I have come to the same conclusions as you and staying long and strong. This has the smell of ultimate price spike in the air ("what uranium should have been or will be one day"), with no meaningful inventories left and a large mismatch between supply (nothing meaningful coming online at short notice) and demand (panic buying from manufacturers, almost no demand destruction via substitution & huge defense spending + now middle east conflict escalating). Wouldn't be surprised if we see $5,000/MTU down the track.

Am here for the EQR re-rate and if we halfway close the gap to the Almonty valuation + EQR keeps executing + tungsten price keeps rising, then there is still a fair bit of meat on this bone left.

Glad you joined the ride in a very timely manner.